Both Wallid and PayPal integrate with WooCommerce and allow customers to pay. On the surface, they appear interchangeable.

Underneath, they are built on entirely different payment architectures.

PayPal is an intermediary-led system built around account balances, internal policy layers, and platform-controlled dispute mechanisms. Wallid is a bank-native gateway built around direct authorization and deterministic settlement at the banking level.

Those structural choices determine how money moves, where risk is absorbed, how disputes are handled, and where transactions can fail.

This article evaluates Wallid and PayPal strictly as gateway models. Not as brands. Not as consumer apps. Not as marketing ecosystems.

If you are evaluating PayPal alternatives for WooCommerce, the real question is not which solution is more recognizable. It is which payment model introduces fewer structural dependencies as your transaction volume grows.

The Core Structural Difference

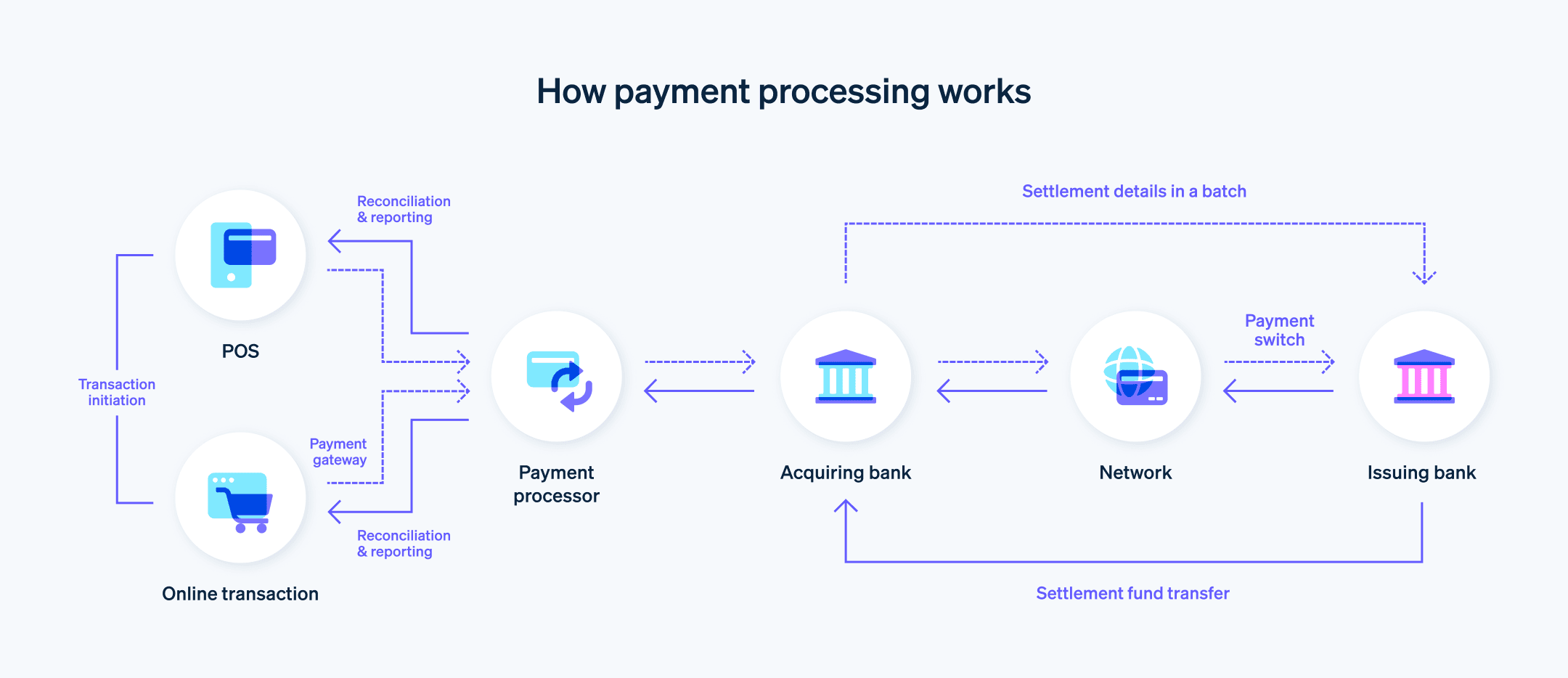

The comparison between PayPal and Wallid begins with how money actually flows.

PayPal: Intermediary-Led Model

PayPal operates as an intermediary. The customer pays into a PayPal account layer. The merchant receives funds inside a PayPal account before transferring them to a bank.

The transaction is therefore account-mediated.

Key structural characteristics:

- Checkout involves a redirect or modal into PayPal’s environment.

- Funds move customer → PayPal → merchant PayPal account → merchant bank.

- The transaction is tied to PayPal account status on both sides.

- Disputes and reversals are processed inside PayPal’s internal system.

This creates a layered transaction stack.

Wallid: Bank-Native Model

Wallid operates as a pay-by-bank gateway. The customer authorises payment directly from their bank. Funds move bank-to-bank without an intermediary wallet layer.

The transaction is bank-native.

Key structural characteristics:

- No account layer between customer and merchant bank.

- Funds move customer bank → merchant bank.

- No wallet balance state.

- No platform-held funds.

The architecture is direct rather than layered.

Money Flow Comparison

PayPal Flow

Customer → PayPal Account Layer → Merchant PayPal Account → Merchant Bank

Failure or restriction can occur at:

- Customer account verification level

- PayPal risk review layer

- Merchant account status layer

- Withdrawal stage

Each additional layer introduces a new dependency.

Wallid Flow

Customer Bank → Merchant Bank

Failure points are limited to:

- Bank authentication

- Bank authorization

There is no separate wallet state or intermediary balance restriction stage.

The difference is not about features. It is about how many entities sit between the buyer and the seller.

Account Dependency vs Deterministic Settlement

A structural comparison of settlement logic clarifies how differently PayPal and Wallid operate:

In PayPal’s model, the transaction is completed inside PayPal before it is completed in the banking system.

In Wallid’s model, authorization and settlement occur directly at the banking layer.

The distinction is structural: intermediary balance state versus direct bank-level settlement.

Disputes and Reversals: Where Risk Is Absorbed

Another structural difference is how disputes are processed.

PayPal

Because PayPal sits between both parties, disputes are handled inside its internal resolution framework.

This allows for:

- Layered reversal mechanisms

- Account-level holds

- Internal balance adjustments

The platform acts as a decision-making intermediary.

Wallid

With a bank-native transaction, dispute handling aligns with banking rules rather than wallet policy layers.

There is no internal wallet balance to freeze.

Risk assessment happens at authorization stage, not via post-settlement wallet controls.

This reduces structural reversibility layers.

Checkout Flow and Conversion Impact

PayPal introduces a multi-step checkout flow.

In most WooCommerce implementations, customers are redirected or prompted to authenticate within PayPal’s environment before returning to the store.

Each additional transition introduces potential drop-off.

For merchants analyzing cart abandonment and payment friction, this structural redirect matters. You can explore broader checkout completion dynamics in Cart Abandonment & Conversion.

Wallid maintains a direct bank authorization flow without wallet redirection layers. The checkout process remains within a single payment authorization sequence.

The difference is not cosmetic. It is architectural.

Reliability: Perception vs Structure

PayPal benefits from strong consumer familiarity. Many shoppers recognize the brand and feel comfortable using it.

That familiarity is perceptual trust.

Structurally, however, PayPal remains an intermediary platform with account-level dependencies and internal policy layers.

Wallid does not rely on consumer brand accounts. It relies on the banking system itself.

The comparison therefore is not about which is "more trusted." It is about which model reduces structural variables.

PayPal vs Bank Transfer Is the Wrong Comparison

Some merchants compare PayPal to manual bank transfer.

That comparison is incomplete.

Manual bank transfer (as covered in Article 6 – Payment Methods & Options) is not a real-time gateway. It requires customer-initiated off-site payment and manual reconciliation.

Wallid is not manual bank transfer.

It is a real-time bank-native gateway that automates authorization and confirmation.

When evaluating a paypal alternative uk or other PayPal alternatives WooCommerce merchants often consider, the meaningful comparison is between intermediary-led gateways and direct bank-native infrastructure.

Which Model Actually Scales?

Scaling payments is less about adding features and more about reducing failure states.

Intermediary-led models introduce:

- Account restrictions

- Wallet states

- Internal policy reviews

- Multi-layer dispute frameworks

Bank-native models reduce:

- Balance holding layers

- Withdrawal dependencies

- Platform-level account constraints

As transaction volume increases, structural simplicity becomes operational leverage.

This is where Wallid positions itself differently in the gateway comparison landscape introduced in the article Gateway Comparison.

Final Perspective: Wallid vs PayPal

Wallid and PayPal are not variations of the same tool.

They represent two different payment philosophies:

- PayPal: intermediary account model

- Wallid: direct bank-native model

If your priority is consumer familiarity inside a wallet ecosystem, PayPal aligns with that objective.

If your priority is deterministic settlement, reduced intermediary layers, and direct bank infrastructure, Wallid is structurally aligned with scale.

To understand the underlying bank-native mechanism in detail, see Article 8 – Pay-by-Bank Explainer.

The decision is not about which logo appears at checkout.

It is about how many systems sit between you and your money.