For high-risk ecommerce businesses, payment processor shutdowns can be just as damaging as losing a major supplier or advertising channel.

Merchants selling peptides, CBD products, supplements, and similar products often face stricter scrutiny from payment providers. A processor may freeze payouts, impose reserves, or terminate an account if it believes the business presents elevated risk.

Understanding why this happens is the first step toward reducing disruption.

This article explains why high-risk ecommerce payment processors shut down merchant accounts, the most common risk factors that trigger reviews or terminations, and how merchants can reduce dependence on traditional card-processing infrastructure through stronger compliance practices and alternative payment methods such as Pay by Bank.

Why Do High-Risk Ecommerce Payment Processors Shut Down Merchant Accounts?

Payment processors may shut down merchant accounts when factors such as business category, product claims, chargeback levels, compliance documentation, or transaction patterns exceed their risk tolerance.

For many merchants, the challenge is not poor business performance but reliance on payment infrastructure that can change its risk policies at any time.

Common Reasons for Payment Processor Shutdowns

High-Risk Product Categories

Certain sectors receive greater scrutiny, including:

- CBD products

- Peptides

- Supplements

- Nutraceuticals

- Age-restricted products

Even approved merchants may face reviews if processor policies change.

Product Claims and Compliance Issues

Claims that suggest medical, therapeutic, or disease-related benefits can increase risk exposure.

Processors often review product descriptions, marketing materials, and supporting documentation when assessing merchants.

Chargebacks and Refunds

High chargeback ratios remain one of the most common reasons for account restrictions.

Processors also monitor:

- Refund rates

- Customer complaints

- Delivery disputes

- Subscription-related issues

Missing Business Documentation

Incomplete websites can trigger compliance concerns.

Important information includes:

- Refund policies

- Shipping policies

- Contact details

- Legal entity information

- Certificates of Analysis (COAs), where applicable

Sudden Growth in Processing Volume

Rapid increases in transaction volume may trigger additional reviews, particularly if the growth appears unusual compared to historical activity.

Why Switching Processors Often Doesn't Solve the Problem

Many merchants respond to an account shutdown by moving to another processor.

However, most card processors rely on similar card-network infrastructure, underwriting standards, and risk-management frameworks.

As a result, the same issues that caused problems with one provider may eventually reappear with another.

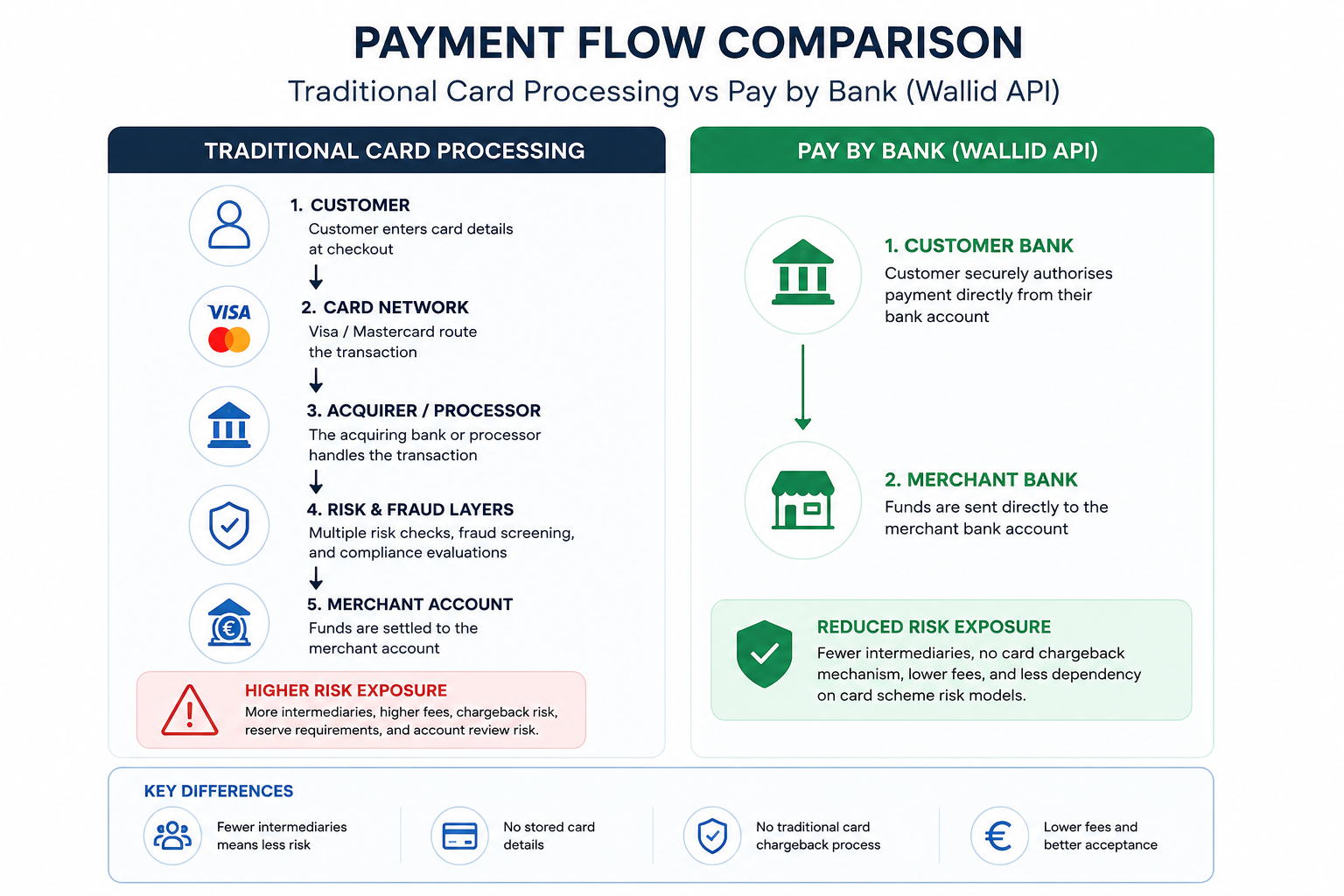

How Pay by Bank Can Reduce Dependency on Card Processors

Pay by Bank allows customers to authorise payments directly from their bank account rather than using card networks.

For high-risk merchants, this offers several advantages:

- Reduced dependence on card-processing infrastructure

- No traditional card chargeback mechanism

- Fewer intermediaries involved in the payment flow

- Alternative payment acceptance alongside existing methods

Solutions such as the Wallid API enable merchants to add Pay by Bank functionality without rebuilding their ecommerce platform.

Traditional Card Processing vs Pay by Bank for High-Risk Ecommerce

The table below highlights some of the operational differences between traditional card-processing infrastructure and Pay by Bank payments.

While Pay by Bank does not eliminate compliance obligations or operational risk, it can help merchants diversify payment acceptance and reduce reliance on a single payment ecosystem.

Payment Processor Shutdown Prevention Checklist

To reduce risk exposure:

- Avoid medical or therapeutic product claims

- Publish clear refund and shipping policies

- Make COAs and supporting documentation available where relevant

- Display legal business information prominently

- Maintain responsive customer support

- Monitor chargeback and refund rates

- Diversify payment methods where possible

While no payment method guarantees immunity from reviews, strong compliance and operational transparency can significantly reduce risk.

Conclusion

Payment processor shutdowns are a common challenge for high-risk ecommerce businesses across the UK and Europe.

Rather than relying entirely on a single card processor, merchants should focus on compliance, transparency, and payment diversification. Adding alternative payment rails such as Pay by Bank through Wallid can help reduce dependence on traditional card infrastructure and improve long-term resilience.